This page has been updated with Workday content and was formerly titled "Renewals vs Supplement/Extensions".

- Overview

- Nanolearning

- Definition

- How to Tell if An Award has Separate Year Accountability

- Outgoing Subaward Award Lines

- HHS Grants and Cooperative Agreements

- Additional Resources

Overview

The concept of Separate Year Accountability (SYA) plays an important role in how GCA sets up a sponsored program award in Workday and how continuation funding will be processed in later years. Understanding this concept can help a department determine whether a future budget period will require a new award line or not and to submit the appropriate request in SAGE.

If you believe a mistake has been made in the setup for Separate Year Accountability, submit an Award Portal ticket under the Award Setup topic.

Nanolearning

Watch this video, developed jointly by Grant and Contract Accounting and the Office of Research’s CORE program, to learn more about this concept and for examples of how it can be utilized.

Definition

“Separate Year Accountability” is defined as the need to keep each year of funding and expenses separated in order to comply with the terms of a sponsored program award.

How to Tell if An Award has Separate Year Accountability

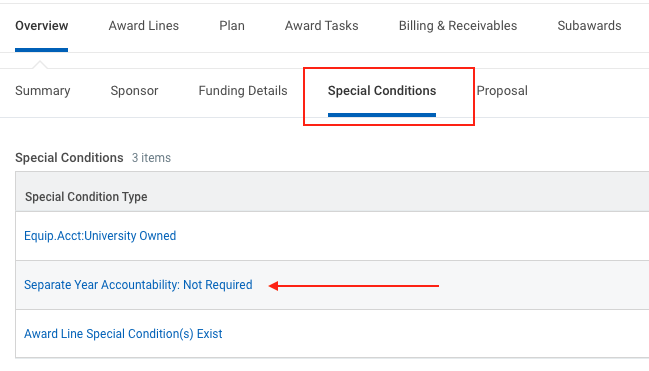

Check Workday

When GCA creates a new award in Workday, they select one of three Separate Year Accountability special conditions based on the terms of that award. You can see these special conditions in the Workday Special Conditions section and in Award Portal.

{kind=link}

{kind=link}

The three special conditions are:

- Separate Year Accountability: Required

- Separate Year Accountability: Not Required

- Separate Year Accountability: Unknown

These special conditions were created in August 2024 and are added to new awards created in Workday after August. The special conditions do not appear in Workday awards that were created prior to August 2024.

Review the Award

If an award does not have a Separate Year Accountability special condition in Workday, review the award document and ask the following questions:

- Does the sponsor require a final report or final invoice at the end of each budget period?

- Does the sponsor restrict carryover for this award?

- Does the sponsor assign a new sponsor award reference number or purchase order number to each budget period?

If the answer to any of these questions is “Yes”, Separate Year Accountability is required. Review guidance on when Separate Year Accountability is required.

If the answer to all of these questions is “No”, Separate Year Accountability is not required. Review guidance when Separate Year Accountability is not required.

SYA: Required

When an award includes criteria that requires Separate Year Accountability, , GCA adds the special condition “Separate Year Accountability: Required” to Workday. Continuation funding then receives a new award line and a new grant worktag. This keeps funding and expenses separated by budget period.

Here are some things to consider when managing an award where Separate Year Accountability is required.

- If you have received an award that provides funding and additional time, submit a Supplement/Extension OSP/GCA MOD. Enter the start date and end date of the new budget period as the Award Line(s) / Budget Period Dates. GCA will review the information and create a new award line and a new grant worktag in Workday.

- If you are waiting for the sponsor to issue the next year’s award or are waiting for the award to be fully processed in UW systems, submit a SAGE Renewal Advance Request to GCA. GCA will then create the renewal advance award line in Workday. Please review the University’s guidance on Advanced Spend beforehand.

SYA: Not Required

If an award does not require Separate Year Accountability, GCA adds the special condition “Separate Year Accountability: Not Required”. Funding and expenses for all budget periods can be combined in one award line and one grant worktag.

Here are a few helpful hints when managing an award that does not require Separate Year Accountability.

- If you have received an award that provides funding and additional time, submit a Supplement/Extension OSP/GCA MOD. Enter the project period start date and end date as the Award Line(s) / Budget Period Dates. GCA will review the information and add funding to the existing grant worktag and extend the award line end date in Workday.

- If you are waiting for next year’s award, submit a Temporary Internal Extension OSP/GCA MOD. GCA will use it to extend the award line end date in Workday. Please review the University’s guidance on Temporary Internal Extensions beforehand.

SYA: Unknown

When reviewing the Award Setup Request and related award document, there are cases where it is not possible to tell whether Separate Year Accountability is required or not. When this happens, GCA will add the special condition “Separate Year Accountability: Unknown” in Workday.

The requirement may be clarified when an amendment to the award is received. GCA will use the criteria to update the Workday special condition as needed. If not, GCA will treat the award as if Separate Year Accountability is not required.

Outgoing Subaward Award Lines

If an award requires Separate Year Accountability, each budget period of the outgoing subaward award will receive a new award line and grant worktag. If the award does not require Separate Year Accountability, only one subaward award line is needed.

Visit GCA’s Subawards webpage for more information.

HHS Grants and Cooperative Agreements

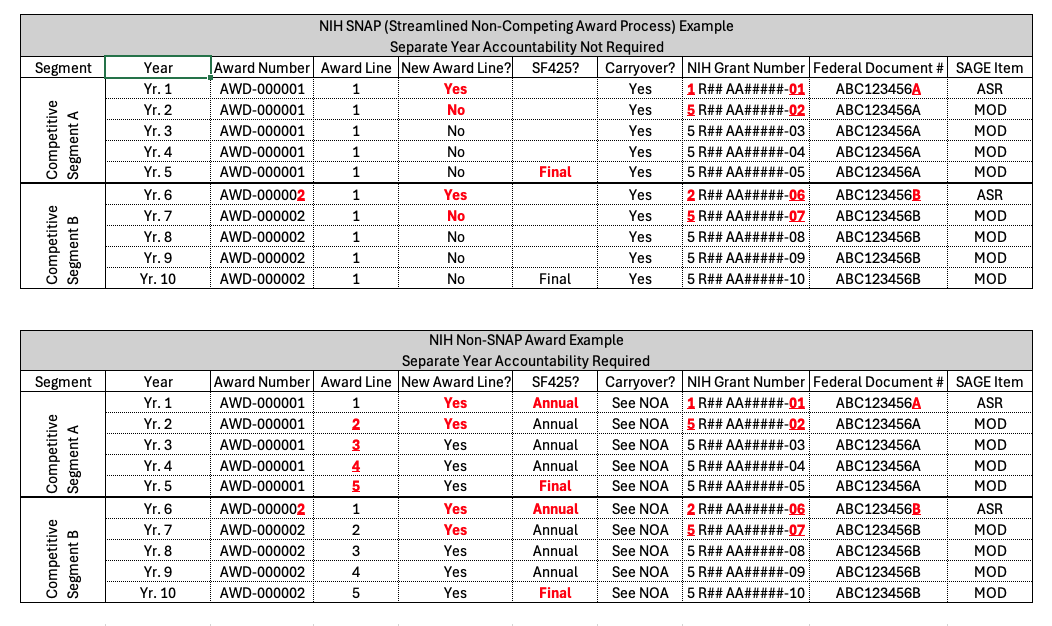

Grants and cooperative agreements from the Department of Health & Human Services (HSS) family of federal agencies, such as NIH non-SNAP grants, typically require a financial report at the end of each budget period and/or assign a different Federal Document Number to each budget period. These awards generally require each budget period to be tracked separately and therefore require Separate Year Accountability.

The following table compares each year of an NIH SNAP award and an NIH non-SNAP award to show how Separate Year Accountability impacts how the awards are set up in Workday.

Additional Resources

- GIM 09 – Advance Spending on Sponsored Awards

- OSP Frequently Asked Question: What is a temporary internal extension?